The idea of supply curve is used in the field of economics. It must be remembered that a curve is a line that allows the graphic representation of a magnitude to be developed according to the values that one of its variables acquires. The concept of supply, on the other hand, can refer to the goods that are put up for sale in the market.

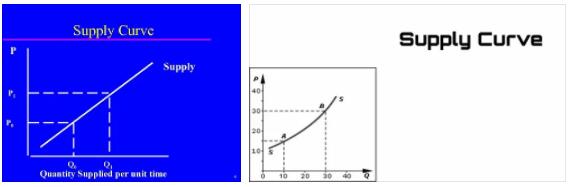

A supply curve, in this framework, refers to the quantity of a certain product that a company is willing to sell at a hypothetical price, keeping all other factors constant that could alter the quantity supplied. There is a direct link between this quantity supplied and the price: the higher the price, the higher the profit for the company, which is therefore willing to sell as much of the product as possible.

- Abbreviationfinder: Find definitions of English word – Aviation. Commonly used abbreviations related to word are also included.

The supply curve, in short, is considered to be of an increasing type, because the higher the price, the higher the supply will also be. It can also be described as concave towards the ordinate axis, and convex towards the abscissa axis; quantities, in this case, are prices.

On a graph, therefore, the supply curve specifies how many products the company intends to offer for each price. At a price P1, the seller is willing to offer a quantity Q1 ; at a price P2, it offers the quantity Q2 ; and so on.

Suppose a pants manufacturer wishes to produce and supply 1,000 pants at a price of $20. If the price rises to $25, the quantity supplied rises to 1,100 pants. At a price of $40, the offer increases to 2,500 pants. All these values, in a graph, allow to obtain the supply curve.

There is also the demand curve, which is defined as the graphic representation of the relationship between the maximum quantity of a given good or service that a consumer would like to buy, and its price. Both curves are key to the theoretical analysis of the economy when studying prices.

From the intersection of the supply curve and the demand curve, the price of the product in the market arises, according to neoclassical economic theory. This intersection also marks the balance between supply and demand.

Among the various concepts related to this topic is elasticity, which can be defined as the percentage by which the quantity of goods offered varies at the time when the sale price undergoes a variation of one percent. Elasticity belongs to the field of economics and its creator was Alfred Marshall, an economist of English origin.

Marshall relied on physics to find this variation (positive or negative, depending on the case) that occurs when one variable changes for another. It is important to point out that the elasticity of the supply curve is linked to several factors, such as the availability of the necessary resources and the technological level of the company.

A nuance that we must clarify is that when we speak of the supply curve, it is understood that the supply to which reference is made belongs to a single company, to the quantities of a product or service and their respective prices; if, instead, the amounts supplied by all firms in a particular market or sector are taken into account, then the appropriate concept is the market supply curve (it could also be industry, depending on the case). This concept, in other words, represents the quantities put up for sale in a given market, at each price.